BYD: The Vertical Integration Machine

The Man Who Beat the Machines

In 1995, Wang Chuanfu was a 29,year old chemist at a government research institute in Shenzhen. Orphaned at a young age in one of China’s poorest provinces, Wang had little capital but immense ambition. He borrowed roughly $350,000 from his cousin, Lu Xiangyang, to start a battery company with 20 employees. At the time, the global battery market was dominated by Japanese giants like Sanyo and Sony, who operated automated production lines that cost tens of millions of dollars. Wang could not afford robots. Instead, he broke the complex manufacturing process down into hundreds of simple manual steps, using cheap human labor and basic fixtures. The result was staggering. A lithium cell that cost Sanyo $4.90 to produce cost Wang’s company just $1.30. By 2003, his startup was one of the largest battery suppliers for Motorola and Nokia.

That company was BYD. When Wang announced he was buying a failing state-owned car manufacturer named Qinchuan Automobile in 2003, investors revolted. The stock plummeted in days. But Wang saw what others did not: the future of transportation was electric, and whoever controlled the battery would control the vehicle. Five years later, Charlie Munger convinced Warren Buffett to buy 10 percent of BYD, calling Wang a combination of Thomas Edison and Jack Welch. Today, the man who could not afford machines has built the most formidable automotive manufacturing machine on the planet. He did it by retaining that initial obsession with cost control, scaling it from handheld electronics to multi-ton passenger vehicles, and ruthlessly integrating every step of the supply chain.

We are examining BYD (OTC: BYDDY) through the Palo Alpha Research framework because the market is currently mispricing the company’s normalized earnings power. A brutal domestic price war and a massive international expansion cycle have temporarily compressed margins and bloated the invested capital base, driving the stock down. However, the underlying industrial machine remains completely intact. As the overseas footprint scales and the energy storage business accelerates, we expect capital efficiency to revert to historical highs. We are long the stock.

Beyond Automobiles: The Anatomy of a Giant

Most Western investors view BYD strictly through the lens of passenger electric vehicles, often framing the company merely as the Chinese rival to Tesla. This is a fundamental miscategorization. BYD is a sprawling industrial conglomerate with operations spanning batteries, semiconductors, electronics assembly, and grid-scale energy storage. The automotive business is the most visible manifestation of the company’s capabilities, but it is supported by a massive, vertically integrated infrastructure that captures margin at every step of the value chain.

The core of this infrastructure is FinDreams, BYD’s umbrella of subsidiaries that manufacture batteries, powertrains, and components. FinDreams operates as an internal supplier but is increasingly selling to external OEMs, providing BYD with scale advantages that pure-play automakers cannot match. Furthermore, BYD Semiconductor is one of China’s largest producers of insulated-gate bipolar transistors (IGBTs) and silicon carbide power modules. When legacy automakers were paralyzed by chip shortages during the pandemic, BYD simply manufactured its own and accelerated its market share gains.

Beyond automotive, BYD Electronics (0285.HK), of which the parent company owns roughly 65 percent, is a massive contract manufacturer. It employs over 100,000 workers dedicated to Apple alone and assembles more than 30 percent of the world’s iPads. On the energy front, BYD surpassed Tesla to become the world’s largest supplier of battery energy storage systems (BESS) in 2025, shipping over 60 gigawatt-hours. The company has secured massive grid-scale contracts, including a 12.5 gigawatt-hour deal in Saudi Arabia and an 11.2 gigawatt-hour deal in Abu Dhabi. This diversification provides BYD with multiple engines for growth and cash flow generation, insulating the parent company from cyclical downturns in any single sector.

The Numbers That Matter: Scale and Compression

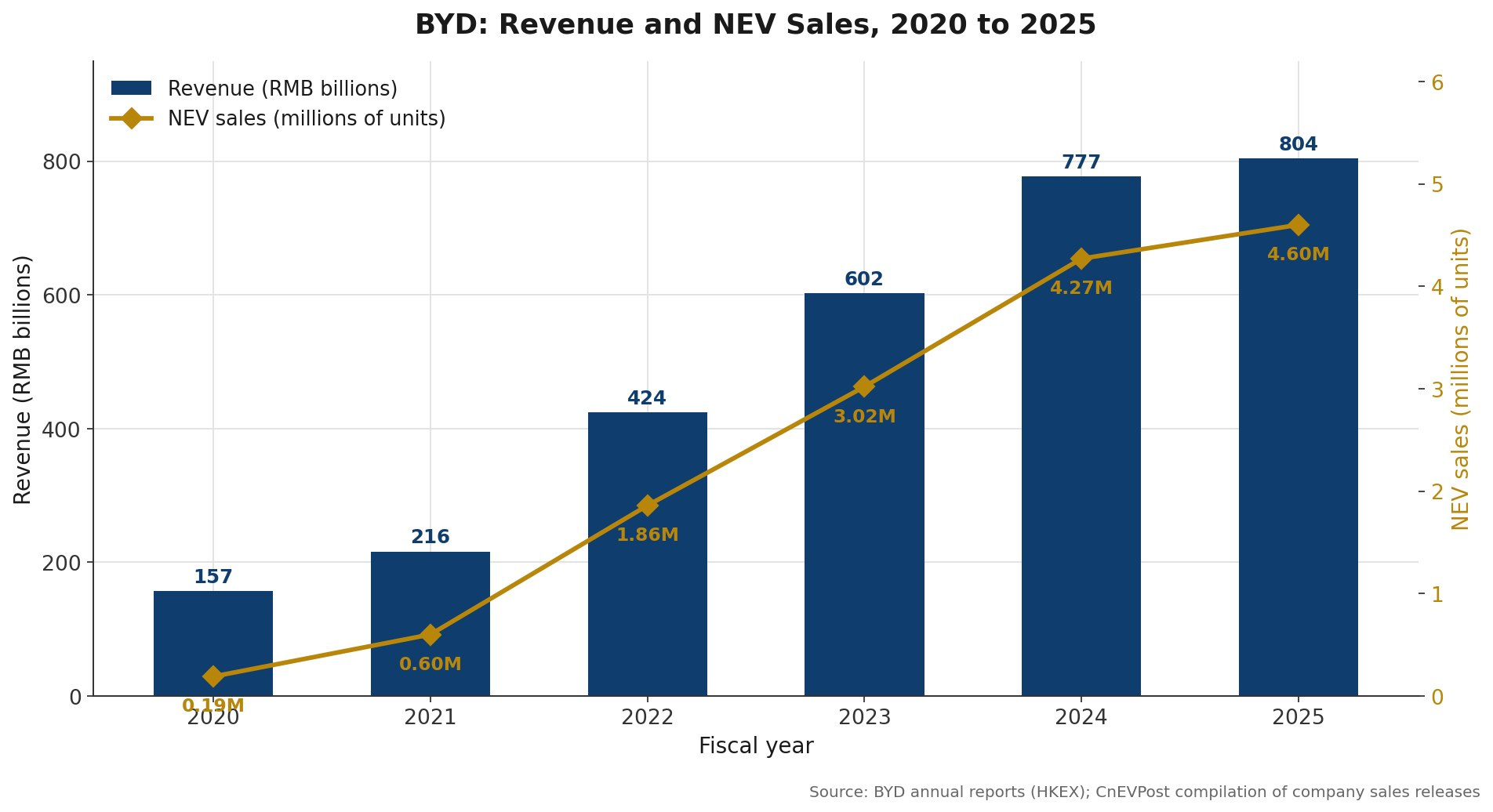

The scale of BYD’s execution is difficult to overstate. In fiscal year 2025, the company generated 804 billion RMB (approximately $112 billion USD) in revenue. Over the past five years, revenue has compounded at an annualized rate of nearly 39 percent, transforming BYD from a mid-tier domestic player into a global juggernaut. New energy vehicle (NEV) sales reached 4.6 million units in 2025, cementing BYD’s position as the undisputed leader in the global EV transition. To put this into perspective, while Tesla commanded a 4.6 percent share of the Chinese NEV market in 2025, BYD held a dominant 27.4 percent retail share.

However, the top-line triumph masks underlying cyclical pressure. The Chinese EV market is currently enduring a brutal price war, driven by overcapacity and a slowing domestic economy. BYD has weaponized its cost structure to participate aggressively in this discounting, prioritizing market share consolidation over short-term profitability. Simultaneously, the company has been transitioning its product lineup to the new Blade 2.0 battery architecture, incurring changeover costs.

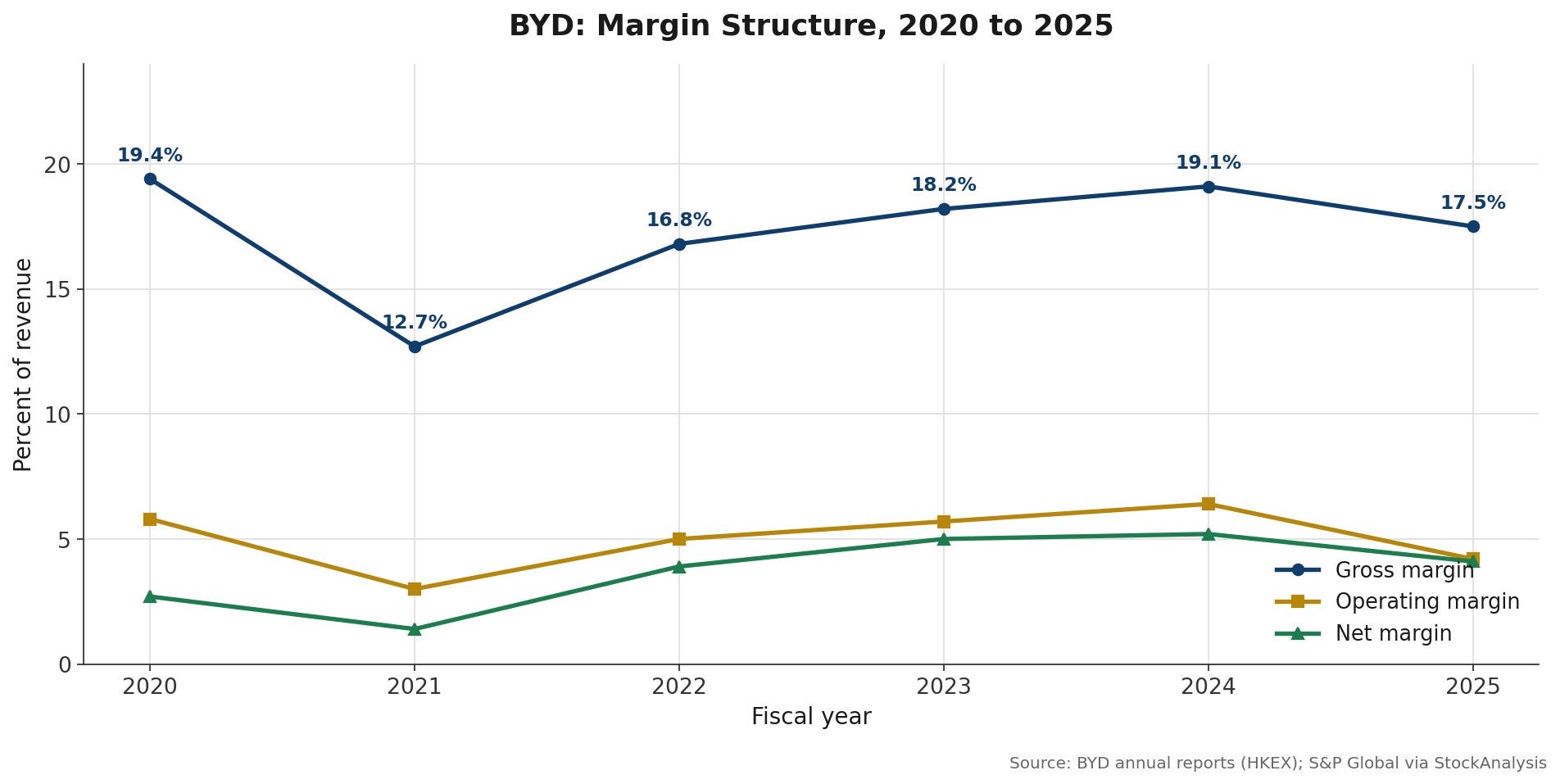

These factors weighed heavily on profitability in the most recent quarters. Operating margins compressed from 6.4 percent in 2024 to 4.2 percent in 2025, dragging net profit down to 33.7 billion RMB. The gross margin profile remained relatively resilient at 17.5 percent, but operating leverage reversed as revenue growth slowed to low single digits while fixed costs remained high. This margin compression is the central debate on the stock today: bears argue it represents a structural deterioration in the face of insurmountable competition, while bulls view it as a cyclical trough before the high-margin export engine reaches scale.

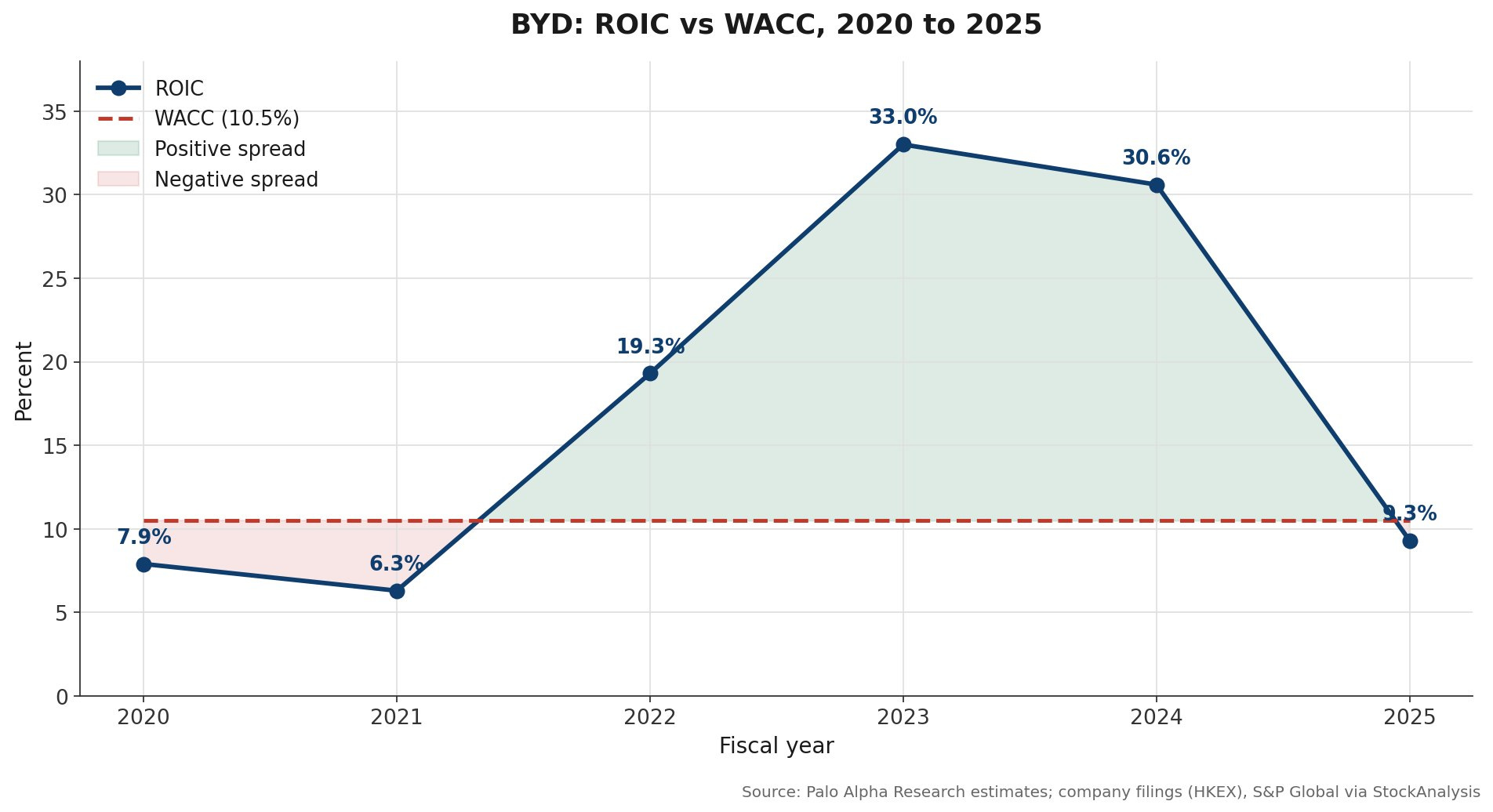

Palo Alpha Framework: The ROIC vs WACC Spread

Our methodology centers on the spread between Return on Invested Capital (ROIC) and the Weighted Average Cost of Capital (WACC). We evaluate every equity position through this lens, as a positive spread is the ultimate driver of intrinsic value creation. We calculate BYD’s current WACC at 10.5 percent. This factors in a 4.6 percent US 10-year Treasury risk-free rate, an adjusted industry beta of 1.10, a standard equity risk premium of 5.5 percent, and a 1.0 percent country risk premium to account for the specific geopolitical and regulatory risks associated with Chinese equities. The cost of debt is highly favorable, with an after-tax rate of roughly 3.0 percent, reflecting BYD’s strong credit profile and access to state-backed financing channels.

Historically, BYD’s capital efficiency has been extraordinary. Between 2022 and 2024, the company generated ROIC prints of 19.3 percent, 33.0 percent, and 30.6 percent. These hyper-elevated returns were not merely the result of high margins; they were driven by a negative working capital cycle. BYD’s massive scale allowed it to stretch payables and force suppliers to finance its growth, keeping the invested capital base artificially low while operating profit surged.

In 2025, the spread inverted. ROIC fell to 9.3 percent against our 10.5 percent WACC hurdle. This compression was driven by the dual impact of the aforementioned operating profit decline and a massive expansion in the invested capital base. BYD aggressively built out overseas manufacturing capacity in Thailand, Brazil, and Hungary. It expanded its logistics infrastructure, including the commissioning of its own fleet of roll-on/roll-off car carriers to bypass shipping bottlenecks. It also reformed supplier payment cycles, reducing the payables float.

We view 2025 as a trough year characterized by pre-productive capital expenditure. The factories built in 2025 will generate revenue in 2026 and beyond. On a normalized trailing three-year basis, BYD generates an average ROIC of 24.3 percent, yielding an exceptional positive spread of nearly 14 percentage points. The industrial machine is merely digesting a massive meal of growth capital; the underlying economics remain highly attractive.

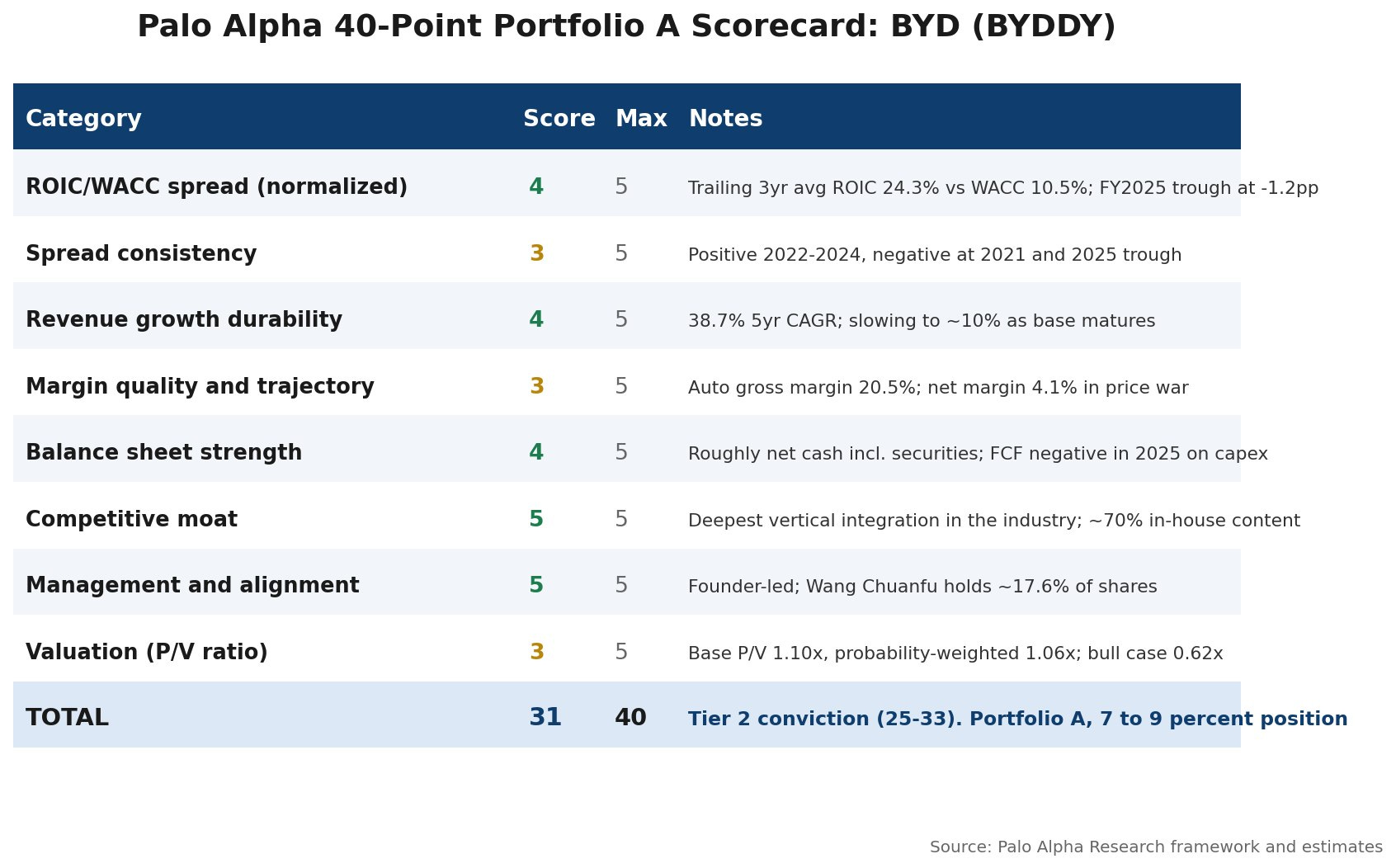

Portfolio A Scorecard Evaluation

Every stock we evaluate must first pass through our 40-point Portfolio A scorecard. We evaluate eight categories, scoring each out of five points. Only companies that pass this rigorous quality filter are considered for core positions. BYD scores a 31 out of 40, placing it firmly in Tier 2 conviction territory.

The scorecard highlights the dichotomy of the current thesis. BYD scores perfectly on competitive moat and management alignment. Wang Chuanfu remains deeply involved as Chairman and President, holding roughly 17.6 percent of the shares, ensuring his interests are aligned with minority shareholders. The balance sheet is robust, operating in a net cash position when including short-term trading securities, though aggressive capex pushed free cash flow negative in 2025.

The deductions come primarily from the current cyclical trough. Margin quality and spread consistency are penalized for the 2025 compression. Revenue growth durability receives a 4 out of 5, acknowledging that the days of 40 percent compounding are over as the base matures, with future growth likely settling into the low double digits. Valuation receives a 3 out of 5, as the stock trades near our base case intrinsic value, offering a reasonable entry point rather than a deep-value fire sale.

The Moat: Absolute Vertical Integration

BYD’s primary competitive advantage is cost leadership driven by absolute vertical integration. The company procures up to 70 percent of its vehicle components in-house, a figure that exceeds even Tesla’s renowned verticality. From mining lithium to manufacturing the battery cells, designing the power semiconductors, building the software, stamping the chassis, and assembling the final vehicle, BYD captures margin at every step of the value chain.

This structure provides a dual benefit. First, it insulates the company from supply chain shocks. When global logistics snarl or component shortages strike, BYD can rely on its internal ecosystem to maintain production lines. Second, it creates a structural cost floor that competitors relying on external suppliers simply cannot match. A traditional automaker must pay a margin to the battery supplier, a margin to the chip designer, and a margin to the tier-one component manufacturer. BYD internalizes all of these margins, allowing it to price vehicles aggressively while remaining profitable.

When BYD engages in a price war, it is weaponizing its balance sheet and integration to bleed sub-scale competitors dry. The current margin compression is a deliberate strategic choice to consolidate market share. By lowering prices, BYD forces weaker EV startups into bankruptcy and accelerates the demise of legacy internal combustion engine vehicles. Once the market consolidates, BYD will be positioned to gradually expand margins on a vastly larger installed base.

Valuation: Three-Scenario DCF Modeling

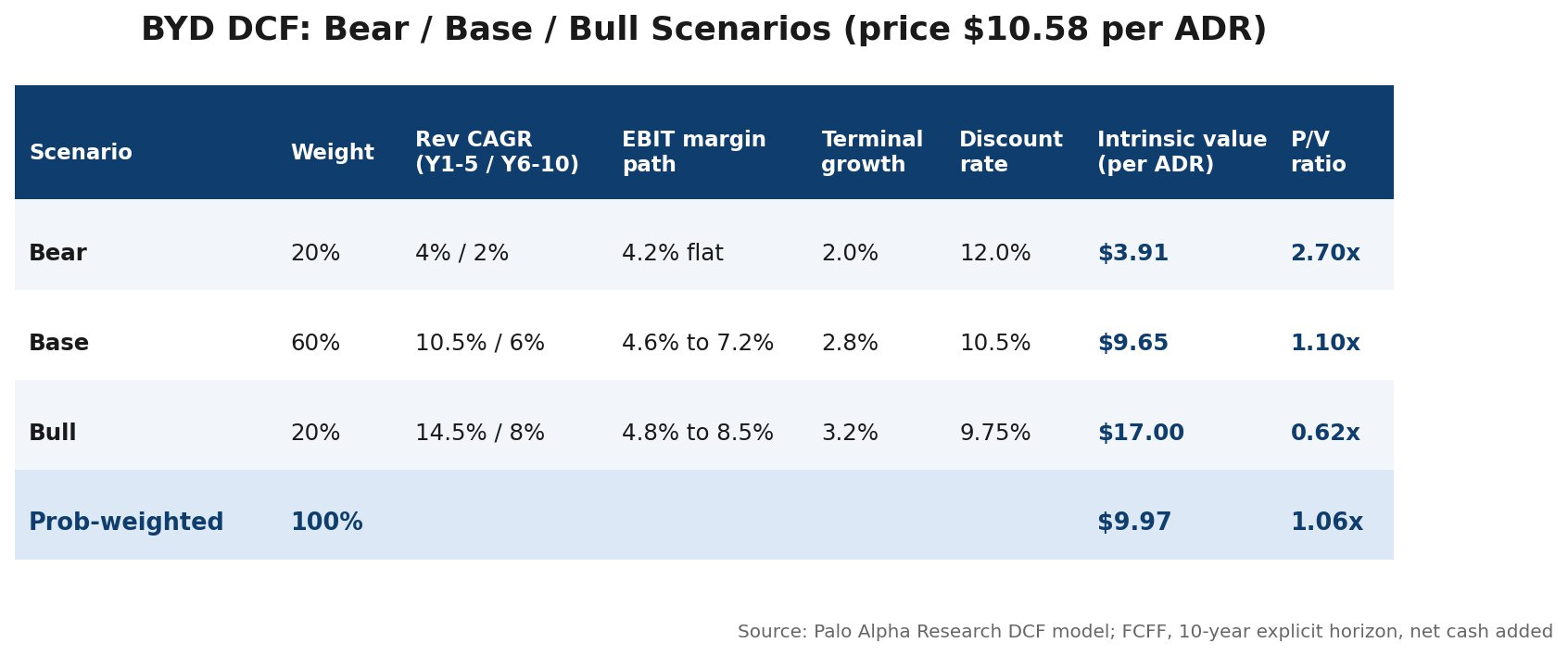

We model BYD using a 10-year explicit Free Cash Flow to Firm (FCFF) DCF, evaluating Bear, Base, and Bull scenarios. Our intrinsic value calculations are presented per BYDDY ADR in USD, utilizing a 7.16 RMB/USD exchange rate. We add back net cash, including short-term trading securities, to the enterprise value.

In our Base case, we assume the 5-year revenue CAGR moderates to 10.5 percent as the domestic market matures, followed by 6 percent growth in years 6 through 10. We model EBIT margins recovering from the current 4.2 percent trough to 7.2 percent, driven by a rising mix of high-margin overseas sales, which typically carry double the margin of domestic units. Using our 10.5 percent WACC and a 2.8 percent terminal growth rate, this yields an intrinsic value of $9.65 per ADR.

The Bear case assumes prolonged domestic price wars and severe tariff barriers stalling the export engine. We model 4 percent initial growth fading to 2 percent, with margins flatlining at 4.2 percent. Applying a higher 12.0 percent discount rate to reflect increased risk, the intrinsic value falls to $3.91. Conversely, the Bull case assumes rapid international scaling and explosive energy storage growth pushing margins to 8.5 percent. With 14.5 percent initial growth and a 9.75 percent discount rate, the intrinsic value reaches $17.00.

Applying a 60 percent weight to the Base case and 20 percent to each tail, our probability-weighted intrinsic value is $9.97. Against a current price of $10.58, this implies a Price-to-Value (P/V) ratio of 1.06x. The stock is essentially fairly valued on base assumptions. We are not buying a deep-value cigar butt; we are paying a fair price for a high-quality compounder, with the international expansion serving as a free call option on the Bull case.

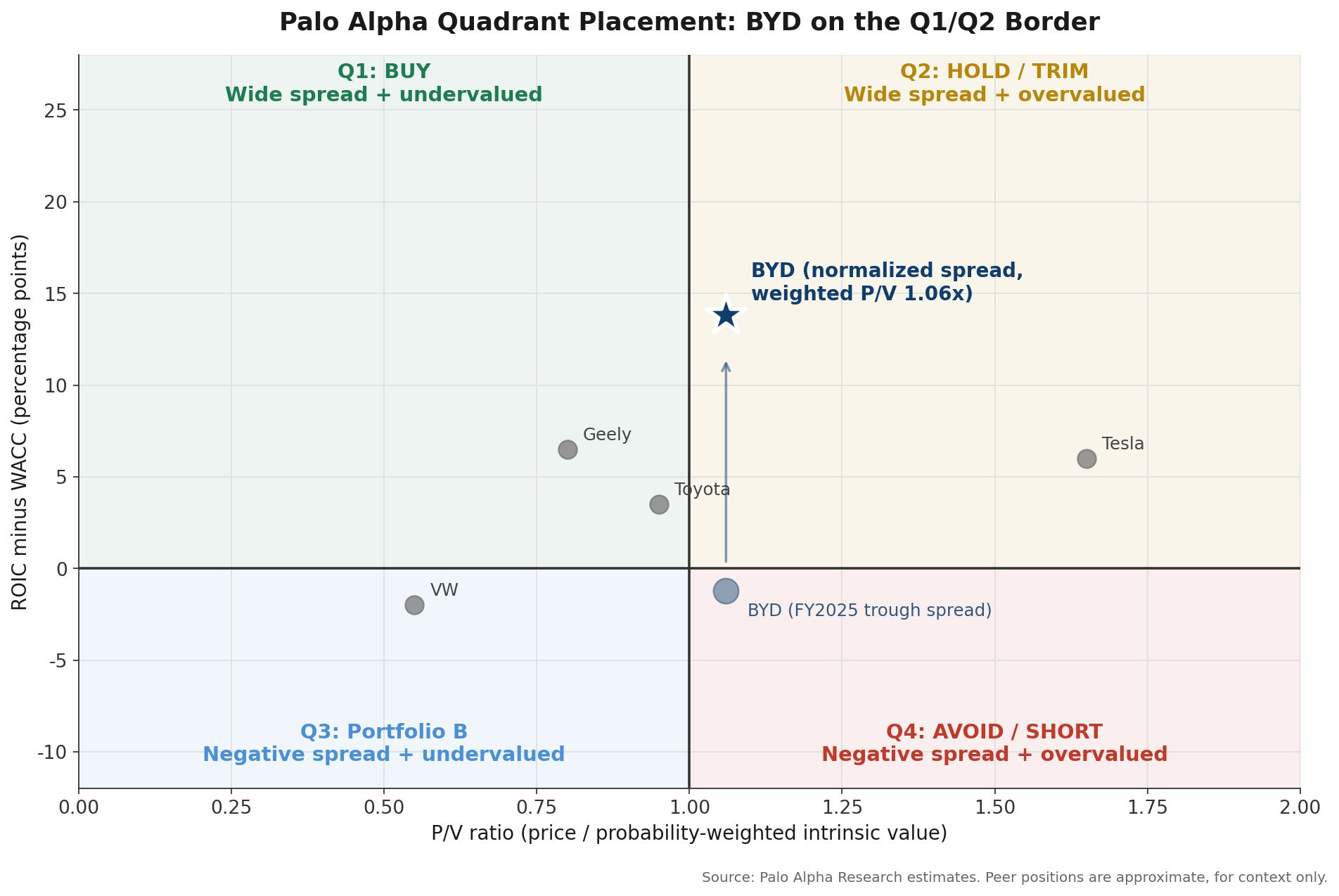

Quadrant Placement: Q1 Compounder

Integrating our spread analysis and valuation, we place BYD on the border of Q1 (Compounder) and Q2 (Trim). Our quadrant framework plots the ROIC/WACC spread on the Y-axis against the P/V ratio on the X-axis. On trough 2025 metrics, the stock sits slightly below the line in Q3 territory, reflecting the temporary negative spread. However, using normalized economics based on the trailing three-year average, BYD is a clear Q1 asset: a wide-moat compounder trading near fair value.

For context, we have plotted approximate positions for peers. Toyota sits in the middle, offering stable but unspectacular spreads. Legacy European automakers like Volkswagen are mired in Q3, struggling with negative spreads and structural bloat. Tesla remains in Q2, boasting strong historical spreads but trading at a significant premium to intrinsic value. BYD offers the most compelling combination of capital efficiency and reasonable valuation in the global automotive sector.

Risks: Tariffs, Geopolitics, and Competition

The primary risks to the thesis are geopolitical and regulatory. BYD is effectively locked out of the US passenger EV market by 100 percent tariffs, removing one of the largest profit pools from its total addressable market. In Europe, the company faces additional EU tariffs of roughly 17 percent on top of the standard 10 percent rate, designed specifically to blunt the cost advantage of Chinese imports.

BYD is mitigating this by aggressively building localized production. A plant in Thailand is already operational, facilities in Brazil and Hungary are ramping up for late 2026 production, and a second European plant decision is imminent. However, localized production carries risks. Manufacturing in Hungary or Brazil will entail higher labor and operational costs than the Shenzhen mega-factories, potentially diluting the overseas margin premium that underpins our Base and Bull cases. Furthermore, political headwinds remain unpredictable; Turkey recently suspended import tax exemptions granted to BYD, stalling a planned factory build.

Domestically, the price war remains vicious. While BYD has the balance sheet to survive, prolonged discounting could delay the margin recovery modeled in our Base case. Additionally, the transition to the Blade 2.0 platform must be executed flawlessly to maintain consumer demand and technical leadership against aggressive domestic rivals like Geely and Huawei-backed brands.

The Palo Alpha Position: Accumulate on Weakness

We are long BYD. Our position rests on the conviction that the 2025 margin compression is a cyclical trough driven by strategic pricing actions and pre-productive international capex, not a structural break in the economic moat. Wang Chuanfu has built an industrial machine that can manufacture complex technology cheaper than anyone else on earth. The vertical integration that allowed BYD to crush Sanyo in the 1990s is the exact same DNA allowing it to dominate the global EV transition today.

As the overseas footprint scales, localized production circumvents tariffs, and the high-margin energy storage business accelerates, we expect operating leverage to return and ROIC to expand back toward the mid-twenties. At a probability-weighted P/V ratio near 1.0x, the market is offering a fair price for an exceptional asset. We view current weakness as an opportunity to accumulate shares of the world’s most efficient automaker. We size BYD as a 7 to 9 percent position within Portfolio A.

Disclosure: Palo Alpha Research is long BYDDY. This article is for informational purposes only and does not constitute financial advice. Do your own due diligence. All intrinsic value estimates are based on proprietary models and publicly available data, including company filings via HKEX, S&P Global via StockAnalysis, and industry reports from CnEVPost and Macrotrends.

Really great read.